20 July 2021

How we’re implementing the GGOB: Profit-Sharing

by Peter Kananen

I’ve long been a fan of the business management and ownership philosophy espoused by Jack Stack in the classic book “The Great Game of Business”. In the book, Jack describes how he grew SRC, a mechanical remanufacturing company, to astounding success by using open-book management principles and teaching every employee in the company how the business makes money. Eventually, SRC embraced employee ownership, providing every employee an opportunity to become an owner of the business. Since 1983, they’ve grown to 1200 employees across over 30 businesses, and have spun out a business consulting company aptly named “The Great Game of Business”.

Why Open Book Management?

Most software designers and developers assume a pretty large amount of transparency from their employers, so open-book management (OBM) to some degree is practiced broadly in our industry. In a consulting company, the dollars and cents of revenue and costs are little more than the bill rates and costs of its employees, so discussing the finances of the business can be pretty revealing as to the realities of the business. One of the fundamental ideas behind OBM is that employees can directly tie their efforts to the company’s success because they should be able to see how the money flows in the business. This requires leadership to intentionally educate the entire team, and it needs to be done in a way that is empowering and tied to their daily work. Combined with a strong sense of purpose and meaningful culture, businesses can increase employee engagement by revealing the financials to everyone.

Profit Sharing was the next step

However, knowing the P&L on paper only goes so far as to achieve results. It turns out that to really change behavior, people need to feel the impact not only in their daily work, but also in the context of their long-term career opportunities, and in their paycheck. At Launch Scout, an obvious next step on our pathway of the GGOB was to put into place a company-wide profit-sharing plan. We’ve talked about doing this for years, but for a number of reasons it hadn’t gotten done. GGOB describes many well-engineered profit-sharing plans that are designed to align individuals, functional areas, and leadership toward a grand yearly goal broken down into quarters. I believe that when we achieve a higher level of organizational maturity, a plan like those outlined in the GGOB could fit us well. But for this year, we needed something simple that we could put into place quickly. Our ownership team spent some time coming up with these simple parameters for our profit-sharing plan:

- Profit needed to be shared immediately following the month in which it was generated

- Profit-sharing could only be done when we had line of sight to positive cash-flow and a reasonably good forecast

- Participation in the plan needed to be as equitable and understandable as possible

How our Profit-Sharing Plan works

If we achieved our goal of constructing a simple plan, then this explanation should read almost like the principles we outlined for the plan.

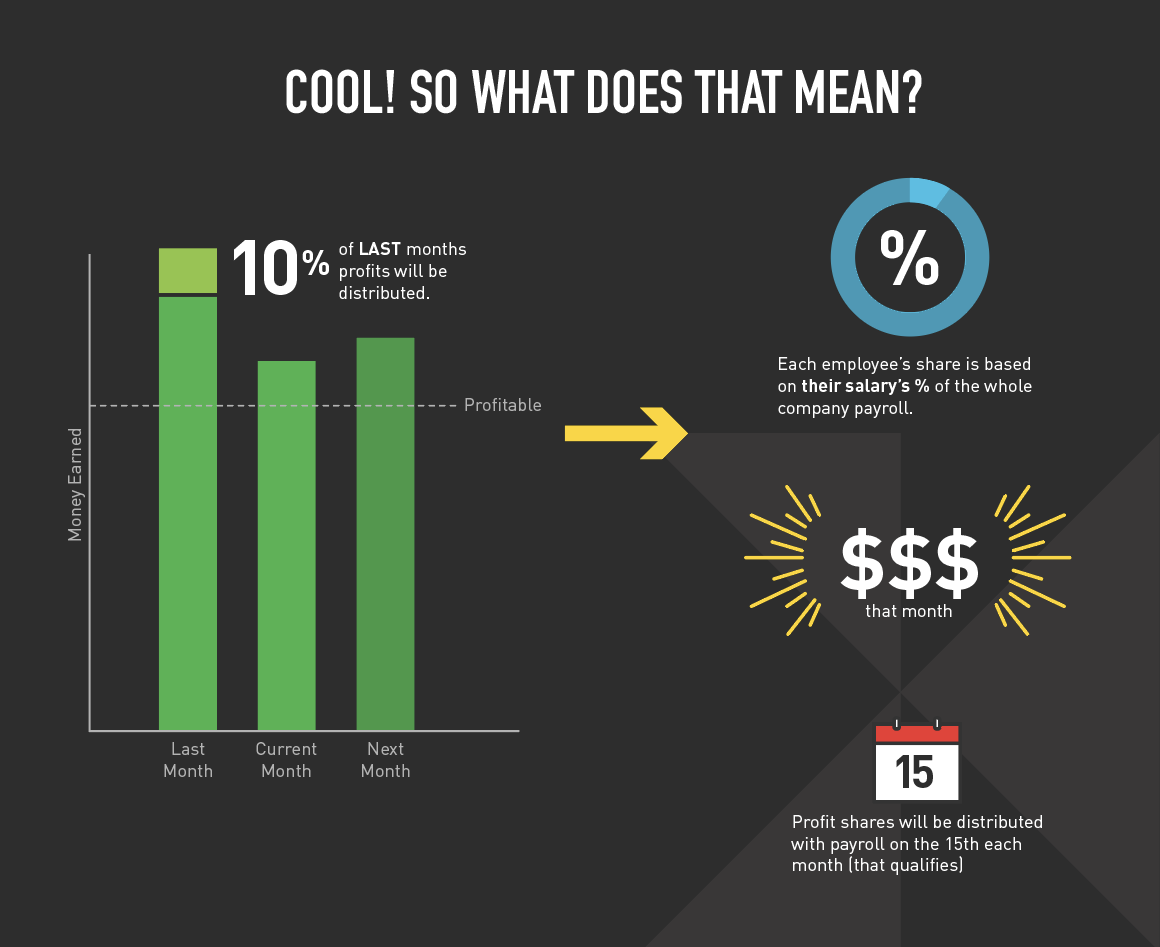

Amount

We’ve set our profit sharing amount to 10% of our pre-tax Net Operating Income amount. This is a starting point - something we could commit to for the long-term but with still plenty of headroom for growth. Once we close the books for a month, we know right away the amount eligible for sharing by just taking 10% of our monthly operating income. The reason we decided to use Net Operating Income as our starting point is that profit-sharing should be a function of our operations, not as a result of other income sources not tied to operations.

Cash-Flow & Forecast

Distribution of monthly profit-sharing has a real impact on cash-flow. Because cash is the lifeblood of any business, we need to ensure that we can afford to pay out our profit-sharing amount. We keep a running metric of our Cash + AR runway, and we make sure that we’re above a 90-day threshold. If we’re not, the profit can’t be shared and is used instead to build our cash runway.

Likewise, it doesn’t make sense to pay out profit if the company expects to lose money in the next month. Because we pay profit-sharing in the month after it’s earned, we need to see that our current month and next month are forecasted to be profitable. If not, the profit can’t be shared and is used instead to shore up our cash runway.

Participation

How each employee participates in a profit-sharing plan can be quite complicated in some plans, and can even be contentious. Setting metrics can lead to unintended consequences, and our goal is to avoid those side-effects as much as possible. We decided that participation in the plan should be defined by just looking at each person’s percentage of total monthly payroll. Presumably, individual compensation is a measure of a person’s contribution to the company’s needs, and therefore should be a good approximation as to what share of the profit they are entitled to. This isn’t a perfect system but it’s clear to everyone in the company, and allows for an upwards trajectory for everyone.

Communication

One of our best assets is our outstanding design team. They came up with this infographic that outlines the plan. Each month we report our financial results, the profit-sharing amount, and whether or not we’ll be paying it based on our cash and forecast.

Next Steps

So, is our intention for the profit-sharing plan working? Well, it’s probably a little too early to say. We still have a ways to go in offering opportunities for everyone in our team to impact our future financial results, but I believe strongly that having the profit-sharing plan in place is a foundational item for our goal of implementing the best practices from the Great Game of Business.

Have any feedback on this plan? Any experiences in how profit-sharing has been implemented at your company? I’d love to hear your thoughts. Send me an email and we’ll set up a time to talk.